Results

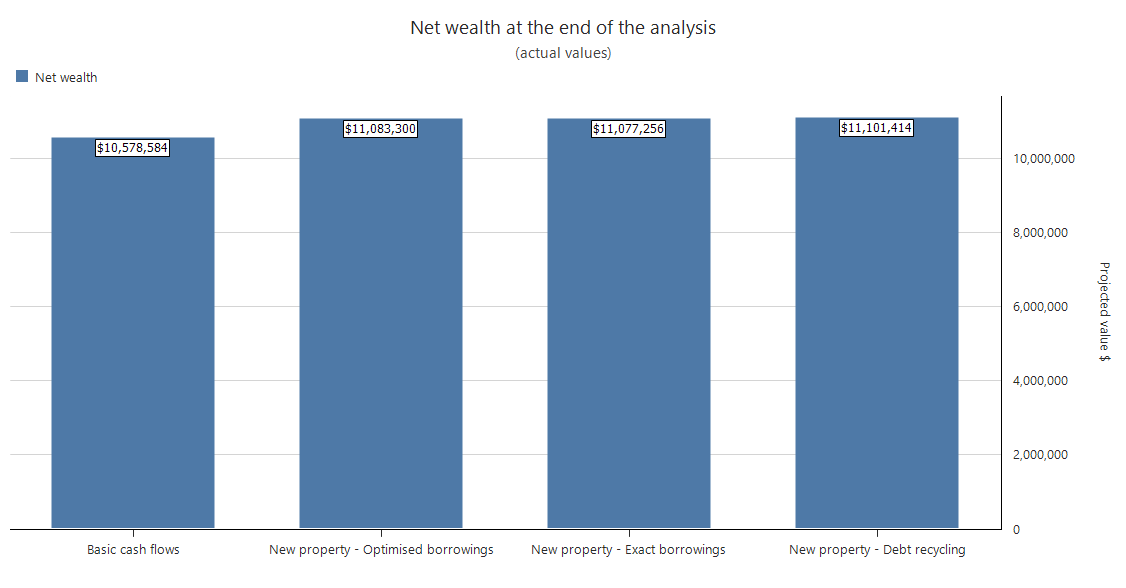

Figure 1: Comparison of projected final net wealth across scenarios

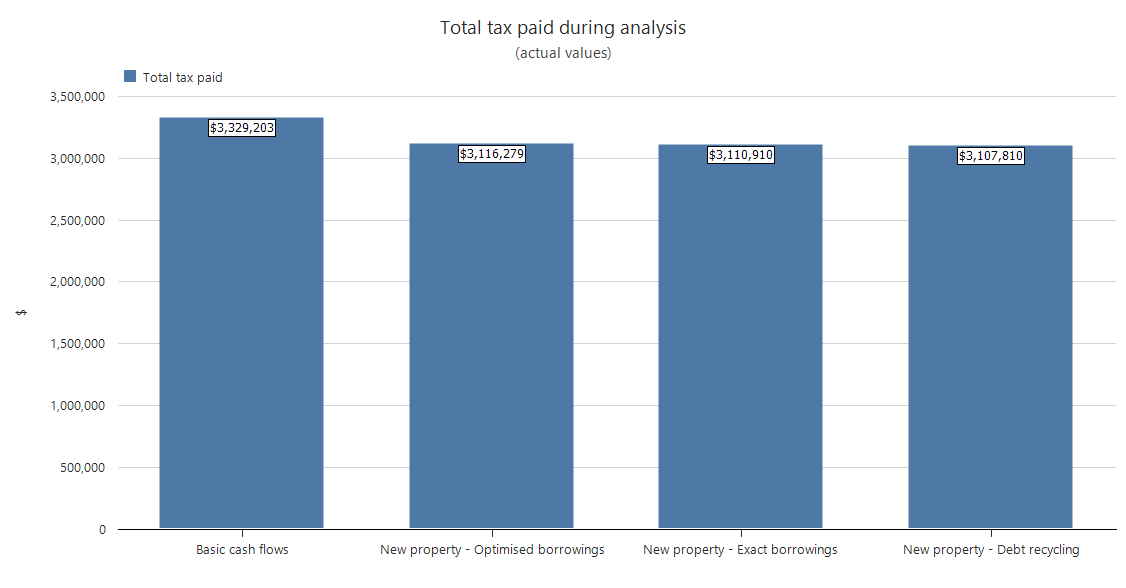

Figure 2: Comparison of projected total tax across scenarios

Scenario | Final Net Wealth | Analysis |

Basic cash flows | $10,578,584 | This baseline scenario allows you to identify the surplus cash, if the couple ‘do nothing’. Each year, the couple have excess cash ranging from $106,000 to $190,000; and by the end-of-analysis, their cash balance is projected to be $1,758,303. This money can be used in alternative scenarios, such as making extra mortgage repayments, or as deposits for new property investments. |

New property – Optimised borrowings | $11,083,300 | This strategy utilises Pathfinder’s optimisation in determining borrowings and repayments for their existing and new properties. Borrowings for new properties:

All loans are feasible: Home loan is repaid in 5 years, and other loans are repaid before the end of analysis. |

New property – Exact borrowings | $11,077,256 | This builds on the prior scenario, but considers a more practical strategy instead of something strictly mathematically optimal – so the projected net wealth at the end of analysis is slightly lower than the previous scenario. Borrowings for new properties:

|

New property – Debt Recycling | $11,101,414 | This more complex strategy boosts the couple’s end of analysis net wealth by about $18,000 to $24,000, compared to the previous 2 scenarios. As well, by focusing repayments towards the Family home loan, it is paid off a year earlier, reducing non-tax-deductible interest – leading to tax savings of $5,400 to $8,500 over 20 years. Borrowings for new properties:

The couple will need to consider whether this marginal benefit is worth the additional effort in implementing the strategy. |